Macro Economics: Economics as a whole includes inflation wage laws and international trade i. e. the whole forest

Micro Economics: Economics as sectors includes supply and demand, market structures and business organizations i. e. one tree

Positive Economics: Statements based on fact and can be proven "Is"

Normative Economics : Statements based on opinion "Should"

Scarcity vs Shortage

Scarce is rare, most fundamental problem to satisfy unlimited demand with limited supply; Shortage is when a product's demand > supply

4 Factors of production:

Land, Labor, Entrepreneurship, and Capital; Human Capital(knowledge) or Physical Capital(tools)

1/6/16

Trade-offs: alternatives that we give up in exchange for something else

Opportunity cost: next best alternative

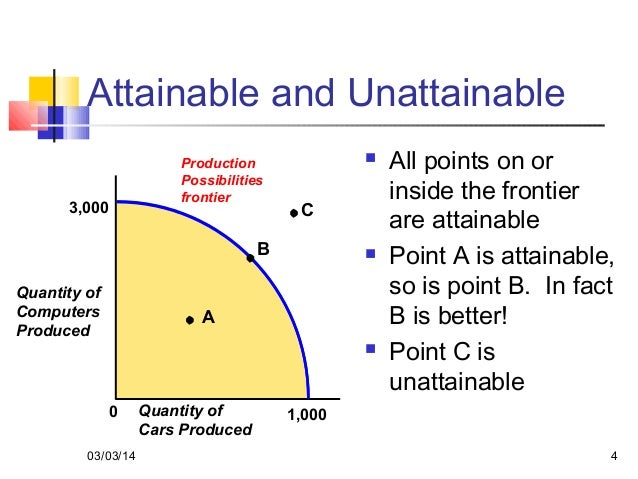

Production Possibilities Graph, PP Curve/PP Frontier:graphs alternative ways to graph use of economics resources has 4 assumptions assigned with it;

- Two goods are being produced

- Fixed resources

- Fixed tech

- Full employ of resources

If a point is on the inside it is attainable and inefficient

If a point is on the PPC/PPF it is attainable, but hard, and efficient

If a point is outside the PPC it is unattainable with this current level of technology and resources

Efficiency: maximizing use of resources

Allocative resources: Satisfying the public with resources

Productive Efficiency: Products are being produced most efficiently and represents a point on the PPC/PPF

Under-utilization: Not using all resources

3 types of movements along the PPG:

1. point moves to the inside

2. point moves along PPC

3. The PPC shifts

1/7/16

6 Causes for PPC to shift:

- Technology increases

- Δ in resources

- Δ in labor

- Economy expands

- Natural Disasters (war/famine)

- Education increases

1/13/16

Price Elasticity of Demand: Measure on how consumers react to change in prices

Elastic demand: E > 1, sensitive to Δ, not a necessity/can be substituted

Inelastic demand: E< 1, not sensitive to Δ, necessity

Unitary Elastic: E = 1

How to calculate PED:

New quantity - old Quantity = Δ% in Quantity demanded

old Quantity

New Price - Old Price = Δ% in Price

Old Price

Δ% in Quantity demanded = Price elasticity of demand

Δ% in Price

1/14/16

Fixed costs/FC: costs that do not change

Variable costs/VC: costs dependent on quantity

Marginal cost/MC: Δ in Price to produce one more unit

MC = New TC - Old TC

Total FC + Total VC = TC AFC + AVC = ATC

TFC / Q = AFC TVC/Q = AVC

TC/Q = ATC TFC = AFC * Q

TVC = AVC * Q TC = ATC * Q

1/15/16

Fire drill

1/18/16

Demand: The # of products people willing or able to buy at various prices

Demand curve always goes down

Law if Demand: Inverse relation of Price to Demand: As price increases, demand goes down. As price decreases, demand goes up

Δ in quantity demand is only affected by Δ in price

Δ in demand has 5 determinants:

- Δ in Buyer's taste

- Δ in # of buyers

- Δ in income (relates to normal goods and inferior goods)

- Δ in price of related goods: substitute goods or complimentary goods

- Δ in Expectations

Normal goods: as income increases, demand increases

Inferior goods: as income increases, demand decreases

1/19/16

Supply: Quantities that producers or sellers are willing or able to produce at various prices

"Supply to the sky"

Law of Supply: Directly proportional relation between price and quantity; as price increases so does quantity, as price decreases so does quantity.

Δ in Quantity supplied is only affected by Δ in price

Δ in supply has 6 determinants:

- Δ in tech

- Δ in weather

- Δ in cost of production

- Δ in # of sellers/producers

- Δ in taxes/subsides

- Δ in Expectations

1/20/16

Peak - Highest point of real GDP, greatest spending, least unemployment, inflation

Expansion - Recovery, real GDP growing, unemployment decreasing

Recession - Real GDP decreasing, unemployment increasing

Trough - Lowest point of real GDP, highest unemployment

No comments:

Post a Comment